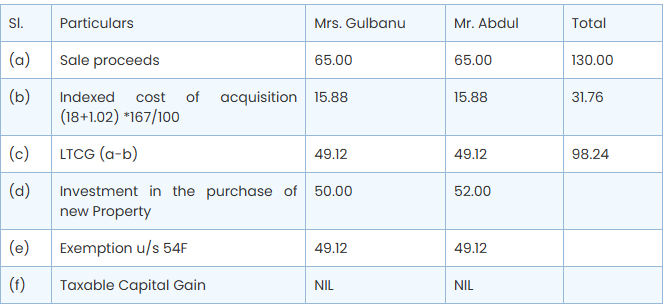

This article delves into landmark judgments clarifying capital gains tax exemptions and related provisions under the Income Tax Act, 1961. Key rulings include the Mumbai Tribunal’s decision in Abdul Nayab Sheik v. ITO (2024), where it was held that capital gains from a jointly owned property are taxable for both owners, while joint ownership in new properties does not affect Section 54F exemptions. In Jitendra V Faria v. ITO (2017) and CIT v. Ravinder Kumar Arora (2012), it was affirmed that full exemptions are allowed even if new properties are purchased jointly, provided the assessee makes the entire investment. Similarly, the Mumbai Tribunal in Shweta Singh v. ITO (2024) ruled that joint ownership of two properties does not bar exemption on capital gains from a separate transfer. Further, the Bangalore Tribunal in Anil Dev v. DCIT (2020) allowed exemptions despite ownership of commercial and joint residential properties, highlighting the importance of factual nuances. Lastly, the Andhra Pradesh High Court in Mir Gulam Ali Khan v. CIT (1986) ruled that legal representatives completing transactions within the stipulated period are eligible for exemptions. These rulings emphasize that joint ownership or legal heirship does not hinder claiming benefits under Section 54F, provided the investments align with statutory conditions. This compilation serves as a practical guide for taxpayers navigating capital gains tax complexities. Let us discuss landmark judgments on some more critical issues : 2. Capital gain from the sale of the property will be taxable in the hands of both the joint owners: Mr. Abdul is the co-owner of a residential house jointly owned by his wife Mrs. Gulbanu Shaikh. This property was purchased in Feb 2002 for Rs 18 Lakhs on which stamp duty paid was Rs. 1.02 Lakhs. He sold the property in Oct 2010 for a sale consideration of Rs. 1.30 crores and purchased two residential Units.-. The first Property is for Rs. 50.00 lakhs jointly in the name of his wife & elder Son Samad and the second property jointly in his name & younger son, Nasir for Rs. 52.00 Lakhs. 2.1 The relevant questions emerged from the above transactions and the answers thereof ,as held by the Mumbai Tribunal in the case of Abdul Nayab Sheik vs. ITO (2024) are as indicated below: – (a) The capital gain from the sale of the property will be taxable in the hands of the joint owners i.e. Mr. Abdul and Mrs Gulbanu. – YES (b) The Addition of the son’s name to the new residential flat would affect his claim of exemption—NO. 2.2 The Capital Gain Tax & Exemption u/s 54F, in the hand of Mr. Abdul & his wife Mrs. Gulbanu will be calculated as follows:

2.3 Conclusion: Both joint owners are individually eligible for exemption U/s 54 of the Income Tax Act, 1961. If the LTCG were taxable solely in the hands of Mr. Abdul, his tax liability would amount to (98.24 – 52.00) Rs 46.24 lakhs.

3. Adding the brother’s name as a joint owner in the new residential property would not impact the exemption under section 54F, provided the entire investment is made by the assessee. Mr. Jitendra is the co-owner of a residential house jointly owned with his wife. He sold the property and invested his share in the purchase of another residential property. The new property was purchased in the joint name of Mr. Jitendra & his brother. However, the entire investment for the purchase of a new residential house, along with stamp duty and registration charges was paid by Mr. Jitendra only.

3.1 It is held by the Mumbai Tribunal in the case of Jitendra V Faria v.ITO (2017), as the entire investment was made by the assessee and only for safety reasons he has included the name of his brother. Mr. Jitendra is entitled to full exemption under section 54F

3.2 Hon’ble Delhi High Court in the case of CIT v Ravinder Kumar Arora (2012) held that the entire investment in new residential property was made by the assessee, he is entitled for full exemption, even though the property was purchased in the joint names of the assessee and his wife.

4. Joint ownership in two residential properties at the time of sale of the original asset would not disentitle the assessee to claim the deduction: Ms. Shweta sold agriculture land and invested the sale proceeds in a new residential flat. On the date of sale, she had two residential properties, jointly owned by her husband and HUF of her father. The first property in which she was residing with her husband, was jointly owned by her husband. A loan was taken from the bank by her husband for purchasing the said property and the said loan was being repaid by her husband. She owned another residential property jointly held with HUF of her father. Thus, on the date of sale of the original property i.e. agriculture land, she did not own any residential house and was only a joint holder in both the residential properties. She is eligible for deduction under section 54F. It is held by the Mumbai Tribunal in the case of Shweta Singh v. ITO (2024) that joint ownership in two residential properties at the time of sale of the original asset would not disentitle the assessee to claim a deduction. 4.1 Joint ownership of a second property is no bar to exemption on transfer of individual property. Merely because the assessee jointly owned another property on the date of the transfer of an asset, its claim for exemption under section 54 could not be rejected in respect of capital gain earned from the transfer of individual property – held by Hon’ble Madras High Court in the case of Dr. Smt. P.K. Vasanthi v. CIT Chennai (2012)

5. Anil sold shares jointly held with his wife, on 03.03.2012, and sale proceeds were deposited in a bank account maintained in the joint name of Mr. Anil & his wife. He has claimed deduction in respect of residential property at Bangalore for which payment was made on 29.03.2011. Although, in the purchase deed, his wife’s name is also there the entire investment was made by Mr. Anil only. He is eligible for deduction under section 54F

5.1 Mr. Anil purchased another property on 11.06.2012 in joint name with his wife. The payment was made from his joint account in which his wife also deposited 50% of the sale proceeds of shares. Mr. Anil’s wife is eligible for deduction under section 54F for the second property.

5.2 In addition to this Mr. Anil was holding commercial property in Chennai. The Assessing Officer disallowed exemption under section 54F to the assessee on the ground that the assessee was the owner of two other residential properties along with one purchased by him out of consideration from the sale of shares. One of those properties was a commercial property and the other residential property was fully owned by the wife of the assessee.: It was held by the Bangalore Tribunal in the case of Mr. Anil Dev v. Bangalore DCIT (2020) that Mr. Anil is eligible for exemption under section 54F

6. Exemption is available if the purchase transaction was completed by a legal representative within the stipulated period of one year: Mr. Khan sold the residential house and immediately thereafter entered into an agreement to purchase another residential house by paying an earnest money deposit. He died four months later, and the purchase transaction was completed by his legal representative within the stipulated period of one year.

6.1 The legal representative of the deceased assesse is eligible for exemption. It is held by the Hon’ble Andhra Pradesh High Court in the case of Mir Gulam Ali Khan v CIT (1986) that the word ‘assessee’ must be given a wide and liberal interpretation so as to include his legal heirs. There is no warrant for giving too strict an interpretation to the word ‘assessee’ as that would frustrate the object of granting exemption and what is more, in the instant case the very same assessee immediately after the sale of the house, entered into an agreement for purchasing another house and paid earnest money and subsequently the legal representative completed the transaction within one year from the date of the death of the deceased. The sale and purchase are two links in the same chain. The lower authorities were, therefore, not justified in rejecting the claim by a legal representative.

Disclaimer: The article is for educational purposes only.

Source: taxguru.in/